What is penny drop verification?

Penny Drop or Bank account verification as is commonly referred to is a way to verify the authenticity of a user’s Bank Account. This is achieved by depositing a small amount (usually a penny and hence the name) – usually INR 1 (one rupee) in the Indian context – which returns the validated bank details along with the beneficiary name.

What is the main purpose of a Penny Drop?

The primary purpose of a Penny Drop is to perform a name and account validation. It answers two critical questions: Is this bank account number active and valid? and Does the account holder’s name provided by the user match the name on the bank’s records?. This helps prevent fraud, errors and mule accounts in financial transactions.

Why do businesses need to verify Bank Accounts?

Penny Drop verification is done for numerous reasons but mostly to verify that the user’s bank account is authentic and that it belongs to the user signing up for the service before transacting on it (e.g. transferring money by businesses). And in India, for many financial services that involve bank account deposits (e.g. Mutual Funds, Insurance, Gaming etc) it is a regulatory requirement to verify users’ bank accounts as part of KYC due diligence.

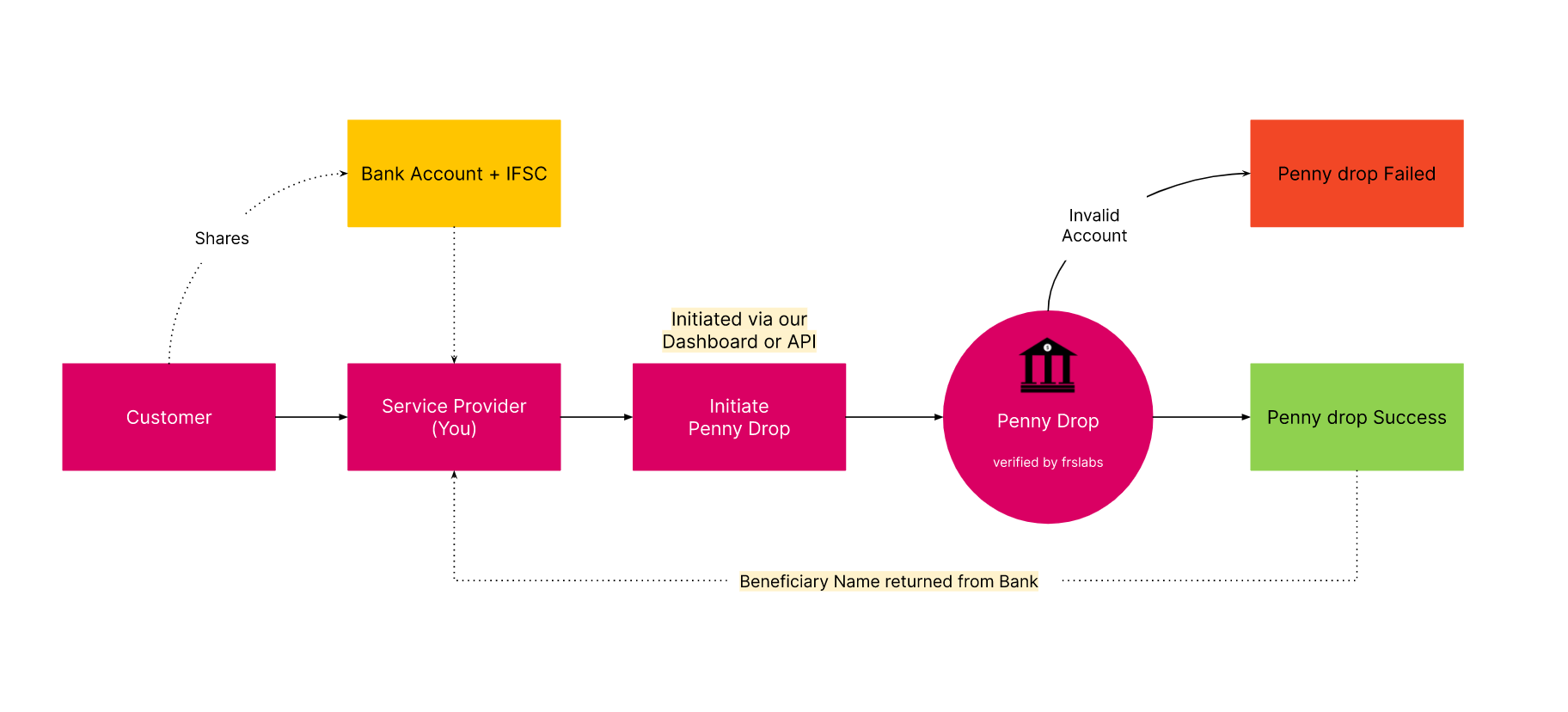

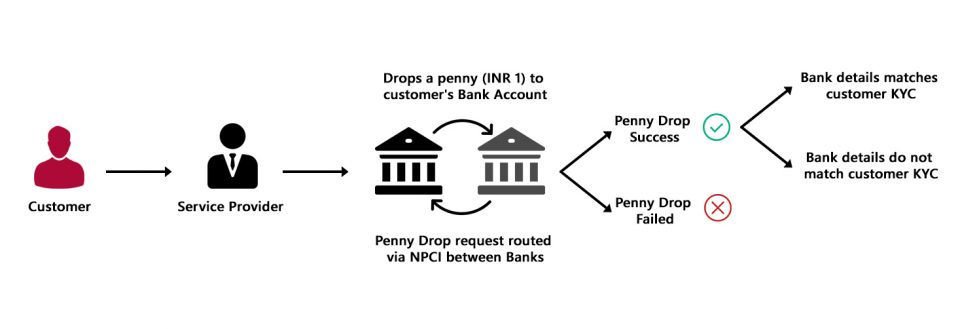

Here’s how penny drop works, in the Indian context.

1) Your customer shares their Bank Account Number and IFSC with You (Service Provider);

2) You invoke our Penny Drop function (through our API or through our no-code Dashboard);

3) Our system drops a penny (INR 1) into your customer’s Bank Account;

4) Penny Drop succeeds (if the Bank Account is valid) or fails (if the Bank Account is invalid/closed);

5) A successful penny transaction returns the verified Account Status and Beneficiary Name. A failed transaction returns just the Account Status and the failure reason.

Additionally, once the verification succeeds, you can compare the identity (KYC) details provided in the application form against the beneficiary name returned from the bank to validate the customer beyond doubt.

Get in touch see how penny drop can be done from a cancelled cheque >

Is Penny Drop or Bank Verification a regulatory requirement?

In April 2020, SEBI (Securities and Exchange Board of India), that regulates securities and commodities market in India, in its KYC circular has specifically recommended verifying Bank Accounts using penny drop as part of onboarding investors by SEBI regulated intermediaries. On 06 October 2020, PFRDA in its VCIP circular mandated instant bank account verification through penny drop to verify the bank account details of the beneficiary. Therefore, multiple regulatory bodies in India have mandated the safe use of penny drop facility to verify customers.

Note: This article was originally published in May 2020. The section below reflects the latest regulatory developments as of April 2026.

The DPDP Act 2023 and What It Means for Penny Drop

India now has its first comprehensive data privacy law: the Digital Personal Data Protection (DPDP) Act, 2023, enacted by Parliament on August 11, 2023, establishes a full framework for how personal data may be collected and used. For businesses conducting penny drop verification, this is directly relevant – bank account numbers, IFSC codes, and beneficiary names are all personal data under the Act.

Pursuant to a gazette notification dated November 13, 2025, MeitY notified the DPDP Rules, 2025, which operationalise the Act in a phased manner. The phased rollout means compliance deadlines are staggered: Rules relating to the Data Protection Board’s constitution came into force immediately upon publication, with Consent Manager registration becoming effective one year after publication, while the substantive compliance obligations come into effect 18 months from notification.

In practical terms, for penny drop: the Rules mandate that consent requests must be accompanied or preceded by a standalone, clear, and plain-language notice detailing the specific data collected and the precise purpose of processing. This means you cannot initiate a penny drop on a customer’s bank account without first presenting them with a properly worded consent notice that names bank account verification as the specific purpose. Our Atlas Privacy Manager platform includes built-in consent capture flows that are aligned with these requirements — speak to us to see how this works in practice.

Penalties for non-compliance are significant: the Data Protection Board is empowered to impose fines up to ₹250 crore per breach.

RBI’s New Beneficiary Name Verification Mandate (April 2025)

A major development in 2025 directly validates the importance of bank account name verification – and expands its scope. From April 1, 2025, the RBI implemented a new system that allows customers to verify the name of a bank account holder before transferring money via RTGS or NEFT – extending to these systems a feature that was previously only available for UPI and IMPS payments.

All banks participating in RTGS and NEFT systems were required to implement this feature by April 1, 2025, making it accessible through internet banking, mobile banking platforms, and branch-based services for over-the-counter transactions. NPCI was tasked with building the underlying verification infrastructure.

What this means for businesses: the regulatory direction is unmistakably toward pre-transaction account name verification becoming a universal standard across all payment rails – not just IMPS-based penny drop. Penny drop remains the most practical and cost-effective method for businesses to verify account ownership at the point of customer onboarding, before any large transaction is initiated.

PFRDA and the Evolution Toward UPI-Linked Verification

PFRDA introduced an advanced mode of bank account verification linking PRAN, PAN, and UPI (VPA) through NPCI, where a subscriber’s PAN and bank account number are sent to NPCI to check if the account is linked with PAN at the bank, returning a binary active/inactive response along with the account holder’s name and UPI ID.

This UPI-linked verification is a complementary method to penny drop, particularly suited to NPS and pension-related use cases. However, it requires the customer to have a UPI ID linked to their bank account — a dependency that penny drop does not have, making penny drop still the most universally applicable method for onboarding customers across banking products, lending, insurance, and gaming.

Is Penny Drop only used for bank account verification?

Primarily, yes. It’s most commonly used for validating savings and current accounts via the IMPS route (provided by NPCI). However, the underlying principle of verification can be applied to other financial instruments, but the term “Penny Drop” is specific to bank account verification.

Where is penny drop services commonly used?

The vast majority of the bank account verifications are done by financial institutions and in particular companies lending to businesses and consumers and gaming companies that will need to make payouts to gamers. The lender can verify that the KYC proofs submitted matches with the beneficiary details obtained as part of the penny drop check. Apart from validating that the KYC details belongs to the right user, bank verification can help cut down on fraud and identity theft whereby the loan is taken on synthetic or stolen identity but the bank account belongs to the fraudster trying to defraud the lender. With just a penny drop, large scale losses can be avoided by the lender.

Penny drop checks have found its way into the insurance industry to verify the bank account details of subscribers before premiums are paid on maturity and at the time of claim settlements. Talk to us about how we help the insurance industry to OCR the cheque details and complete penny drop verification in a single non-intrusive step.

Besides, penny drop verification is useful for businesses of all shapes and sizes. For example, an organisation with just a few employees can verify their Bank account details through a penny drop. This will ensure that the Account holder is the same person employed (you’d be surprised how many aren’t) before beginning to transfer salaries and expenses. Imagine salaries or expenses going to the wrong accounts or failing to be transferred and the resulting stress for both the employer and the employee. In addition, penny drop checks can also be used for age verification, as opening a bank account requires the account holder to be over 18.

Did you know that bank verification as part of your employee background checks are exorbitantly high? As high as 20 times what we normally charge for a Penny Drop transaction. Next time when you want to verify your employees’ bank accounts, simply sign into our dashboard (no code and no set up or training needed), upload your employee bank account details and have them verified instantly at 1/20th the cost of what background verification companies currently charge.

Learn more about about PAN Verification, Penny Drop and Name Check as part of your KYC >

How do I initiate a penny drop check for my customer?

Let’s take a real-life example. Let’s suppose you want to verify the Bank Account of your prospect before onboarding as a customer.

Step 1:

You will need to request the following details from your User prior to verifying the bank account.

1) The Bank Account Number

2) The IFSC Code

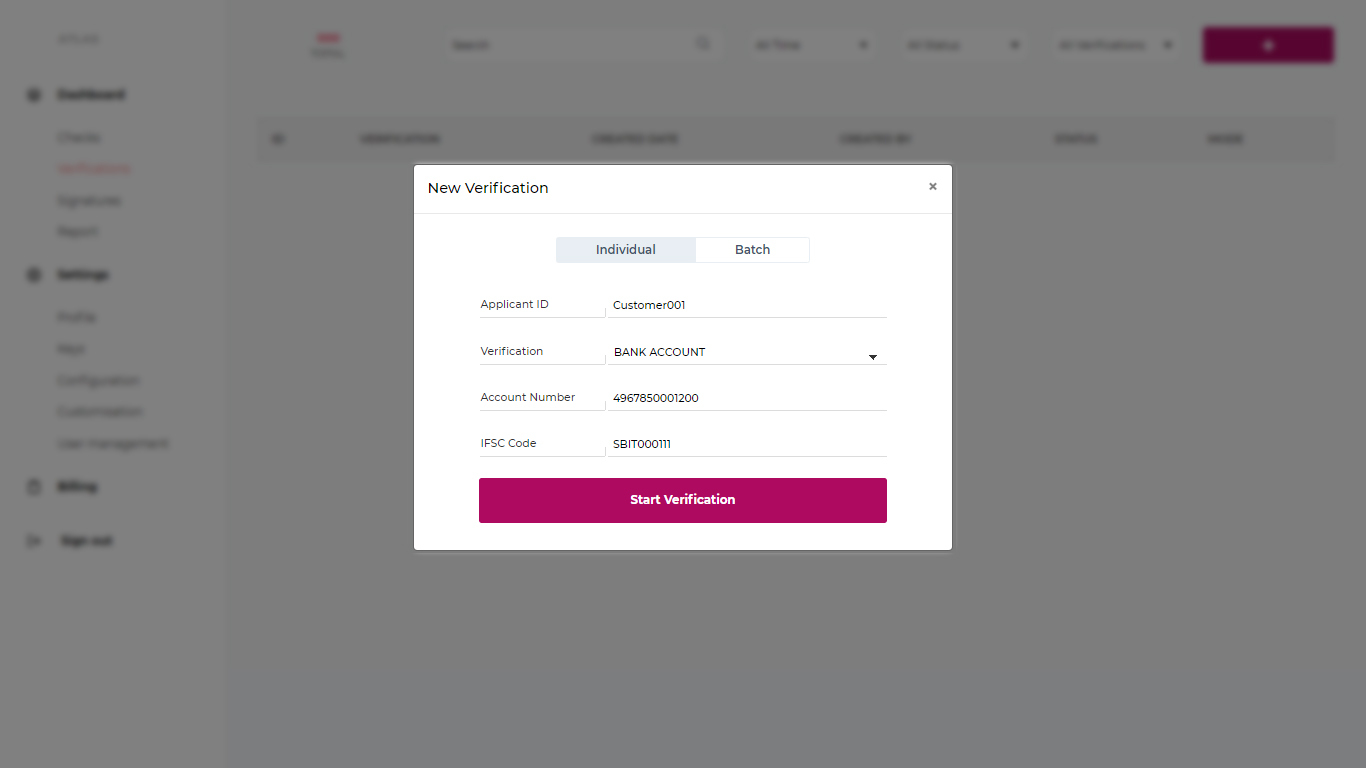

Step 2:

You can use the our dashboard to instantly do a penny verification. This does not require any integration or coding on your part. Once you login, you can simply complete the penny drop verification instantly. Please book a demo today so we can show you exactly how this is done.

Note that you can do verification for a single person or entity or you can upload several thousand bank accounts at once to do a batch penny drop verification using the no code Atlas Dashboard.

As you can note, you can do an individual penny drop check or if you have a number of customers who have submitted their bank account details, you can do a bulk or batch penny drop check. All of the details can be viewed in the dashboard and can be downloaded to your own server once completed.

See how you can use penny drop as part of Video KYC (VCIP/VIPV) >

What is the technical flow of a Penny Drop transaction?

When you initiate a penny drop, your system sends the customer’s bank account number and IFSC code to our API. Our system then routes a real-time INR 1 transfer via the IMPS network through one of our banking partners to the destination account. Within seconds, the bank returns a response confirming whether the account is active and valid, along with the registered beneficiary name, which you can then match against the name provided in the customer’s application or ID proof.

What does a “Name Mismatch” result mean?

A name mismatch occurs when the beneficiary name returned by the bank does not match the name provided by the customer in their application or on their ID document (such as PAN or Aadhaar). This could be due to a spelling variation (e.g., “Mohammed” vs “Mohammad”), a name order difference (first name and last name swapped), or in more serious cases, an indicator of potential fraud or identity theft. Our API supports fuzzy name matching logic to handle common variations, and you can configure the match threshold to suit your risk policy – so genuine customers aren’t unnecessarily rejected.

Can Penny Drop verify joint accounts?

The response from the bank typically contains the primary account holder’s name. Verifying a joint account can be complex as the name matching logic needs to be configured to check against multiple names. It’s best to discuss specific joint account use cases with our team.

How can I integrate Penny Drop APIs within my own Application?

If you are interested to integrate our APIs into your own web or mobile application, you can follow these steps.

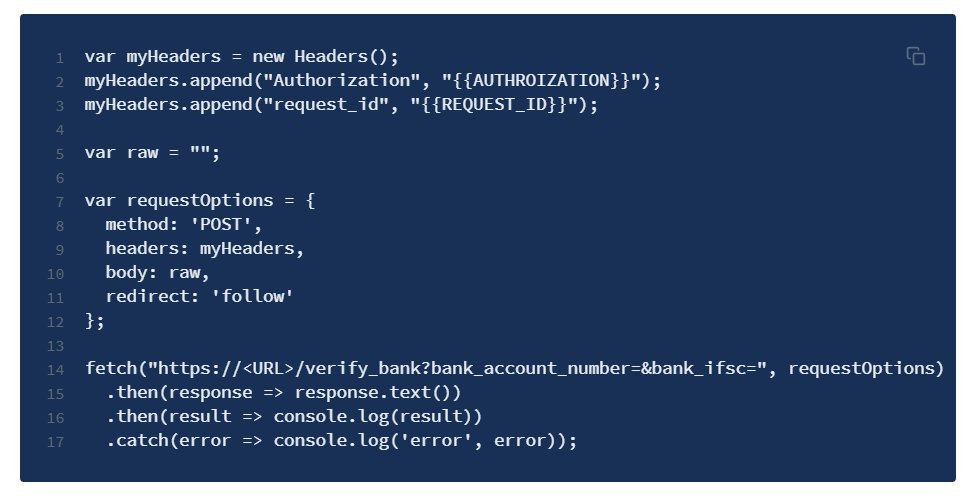

Step 1:

Once you have the Account Number and the IFSC Code, you will need to make an API call to our server. Don’t be alarmed, APIs are your friends whereby just a few lines of code in your server (you can use the sample code already available to build yours) and you can complete this in no time.

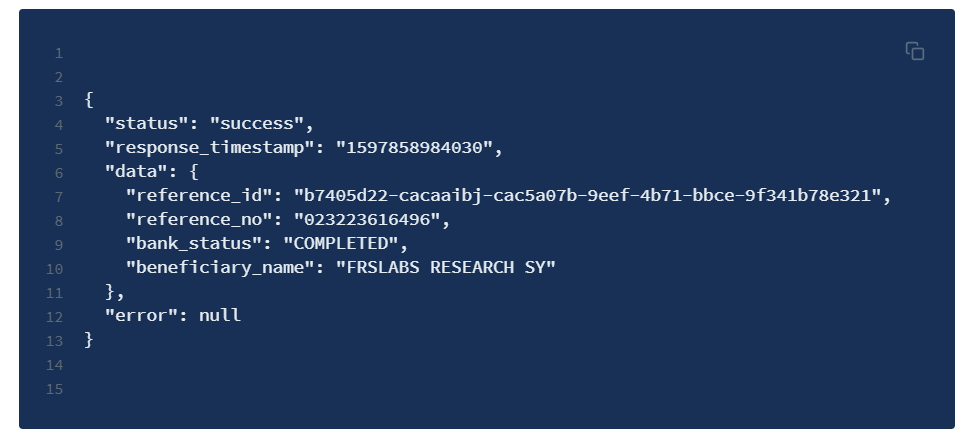

Step 2:

Once an API call is made, it will return a response. The response will usually be in the form of JSON which your Application can now handle. For example, if the Bank Account is valid, it will return the Bank Details, Beneficiary Name and a Success status. If the Bank Account is invalid, it will return an error code along with the reason why it had failed.

That’s it. In just a few steps, you will now be able to verify the details of your users before you onboard them. You can go one step further by matching the beneficiary name with the name in PAN or Aadhaar to verify the true identity of the beneficiary.

Did you know that penny drop verification can now be integrated as part of your Video KYC flow. During the video call, you will need to capture a picture of a cancelled cheque. And our technology will make a penny drop API call to extract the account number and IFSC code and complete the verification while you are still on the call. Discover our cutting edge assisted video kyc and unassisted video kyc that can drive 10X growth. You can be a business of any size and onboard customers from anywhere in India. Request for a free trial so you can see for yourself.

How safe is penny drop done through frslabs?

Our Bank Verification now comes with built-in fraud protection. Penny Drop check is achieved by dropping INR 1 into the Bank account of a beneficiary (e.g., a customer who is onboarding for your services) to verify that the Bank Account indeed belongs to the customer and the beneficiary name matches with the proof of ID submitted by the customer. As there is physical money deposited to verify Bank Accounts, some customers (rather fraudsters) took advantage to transfer large sums by doing penny drop transactions several times, defrauding tens of thousands of rupees. We have devised a built-in trip circuit to cut this fraud out. Book a demo to see how we fight penny drop fraud and help you succeed without wasting a penny.

Do you have a need for Penny Drop and Name Match as part of your verification?

Our Advanced Bank Verification API allows you to complete a penny drop and also do a name match to verify the legitimacy of the account holder against Application and ID names. You can verify up to 3 names against the Bank Beneficiary name as part of a single API call. For example, you can match the Application name and/or National ID name versus the Bank Beneficiary name to verify the legitimacy of the customer. As you can do this in one go, you will save on your penny drop and ID verification costs.

Can I verify a Business Bank Account?

Yes indeed. This is just the same as verifying an individual bank account. In the case of a business bank account, the response returned will be the name of the business, for example FRSLABS RESEARCH SYSTEMS PVT LTD. Also note that unlike personal accounts, if there are multiple account holders or signatories, those account holder details are not revealed in the response – only the business name is passed back as beneficiary name in the Penny Drop API or Dashboard response.

How secure is penny drop verification?

We use advanced fail-safe relays from multiple banking partners to complete penny drop transactions. We use SHA-256 to encrypt the entire payload from your server to our server and through the IMPS system, providing you with the response back through the same secure channel. We do not store your responses once the API response is completed. If you are using our dashboard, you have the option to store the data, which is securely stored in dual-zone RDS in AWS South (Mumbai and Hyderabad Region). None of our engineers have access to your data, which is protected through strict access controls and IAM configurations.

Is the Penny Drop process secure and compliant?

Yes. Every penny drop transaction is conducted over an encrypted channel using SHA-256, and the INR 1 transfer is processed through the regulated IMPS network via RBI-licensed banking partners. From a compliance standpoint, penny drop is explicitly recognised by SEBI, PFRDA, and other Indian regulators as an approved method of bank account verification for KYC purposes. Under the DPDP Act 2023, consent must be obtained from the customer before their bank account details are processed — our platform includes built-in consent capture to keep you fully compliant.

What are the key benefits over manual bank account verification?

Manual verification – such as physically examining a cancelled cheque or waiting for a micro-deposit confirmation that the customer must report back – is slow, error-prone, and adds friction to the onboarding journey. Penny drop verification is instant (results in seconds), fully automated, and directly validates the account against the bank’s own records rather than relying on the customer to self-report. This eliminates human error, reduces turnaround time from days to seconds, and significantly lowers the risk of fraud from forged cheques or misreported account details.

Beyond Financial Institutions, who else uses Penny Drop verification?

Its use is widespread across industries:

Fintech & Neobanks:For seamless user onboarding.

E-commerce & Marketplaces: To validate seller and vendor bank details for payouts.

Gig Economy Platforms: To ensure accurate payroll for freelancers and contractors.

Insurance Companies: For validating details before claim settlements.

Mutual Funds & Wealth Tech: For validating investor bank accounts.

Employee Onboarding: Verifying the bank accounts of employees.

Vendor Payments: Companies verifying the vendor before making payments.

Does the penny drop always return responses in real time?

For 99% of cases, responses are received instantly within a few seconds. However, after completing nearly 10 million bank verifications, we’ve observed that a small percentage of checks take longer than a few seconds, sometimes from a couple of minutes to an hour. The reasons vary, including issues with the receiving bank not functioning as intended, which leads to delays, or severe congestion in the IMPS network, resulting in longer response times.

Our penny drop service is built using multiple backend relays. If we anticipate a delay of more than 30 seconds, we automatically attempt the penny drop with another relay. In cases where a real-time penny drop is not possible, even with multiple relays, we offer a status check feature to confirm whether the penny drop has been completed. This allows your processes to continue without waiting for the penny drop results.

However, if your processes require real-time responses and are waiting for a definitive result, there may be a slight impact on user experience. Please reach out to us if you need strategies to manage such situations, which go beyond the technology layer and involve the IMPS network and partner banks participating in the network to provide results.

Is consent mandatory for doing penny drop?

Absolutely yes. With the release of the DPDP Act 2023, it is incumbent on the verifier to ensure that informed consent is obtained before initiating penny drop verifications. This will ensure that you are on the right side of the law. We help you comply with a simple consent notice presented before you collect the bank account details from the customer. Please talk to us to see how you can integrate consent notices to penny drop verifications.

How does Penny Drop help in reducing transaction failures?

A large proportion of failed payouts – whether salary transfers, loan disbursements, insurance claims, or gaming withdrawals – occur because the destination account number is incorrect, closed, or dormant. By running a penny drop check before any significant financial transaction, you validate the account is live and the beneficiary name matches your records, catching errors at zero cost before they become costly failures. This is especially valuable for businesses processing high volumes of outward payments, where even a 1–2% failure rate can translate into significant operational overhead and customer dissatisfaction.

What is the success rate of a Penny Drop?

The success rate is very high for valid, active accounts. The main reasons for an “unsuccessful” or “invalid” response are a wrong account number, an incorrect IFSC code, or a dormant/closed account. This is really why we are verifying the bank account before you make any large scale financial transaction and avoid fraud and errors.

How much does penny drop cost?

Penny drop pricing is based on your volumes as they are discounted at large volumes by partner Banks. All our pricing is transparent and provided to you upfront without any hidden fees and you will only be charged for successful penny drop transactions. You can view your penny drop statement in real time from our dashboard so you know exactly what you are paying for. Please get in touch with us so we can understand your needs and share our pricing and provide you with trial access to try penny drop before you buy.

Did you know that other than Bank Account Verification (Penny Drop) we can help you with a host of other Indian ID verifications such as Voter ID, Driving License, GST (Business Verification), MSME, Director, FSSAI etc. These ID verification APIs are easy and simple to integrate (or can be used with our dashboard without integration) at very low costs. Please do checkout all of our verification services that we provide to verify Indian individuals and businesses.

Bank Verification (Penny Drop)

Verifies the legitimacy of the Bank Account (for all Bank Accounts in India) by dropping INR 1 into the beneficiary’s Bank Account. The verified Bank Account will return the beneficiary’s name.

PAN Verification

Verifies the legitimacy of the Permanent Account Number (PAN) against the issuing authority (Income Tax Department of India). Read more about PAN verification >

PAN KRA Verification

Verifies whether a given PAN number is registered with any of the KRA (Know your customer Registration Agencies in India). If the PAN is enrolled with any of the KRAs it will bring the enrolment status of the customer.

GST Verification

Verifies the legitimacy of the Goods and Services Tax Number (GST) against the issuing authority (GSTIN). Verified GST numbers returns the full business details for the input GST number.

Voter ID Verification

Verifies the legitimacy of the Voter ID (EPIC – Electors Photo ID Card) against the issuing authority.

Driving Licence Verification

Verifies the legitimacy of the Driving License against the issuing authority (Parivaahan). Verified Driving Licence returns the demographic details and the photo of the driver.

Passport Verification

Verifies the validity of the Passport number. Note that this is applicable only for Indian passports which has a File Number printed on the back page of the passport.

Company Verification

Verifies the Company Name/CIN and returns relevant details like Company Data, Director details and Charges existing on Company/LLP.

Director Verification

Verifies the DIN and PAN of the Director and if valid, returns the relevant details with match status as True or False respectively.

FSSAI Verification

Issued by the Food Safety Association of India, this helps verify the FSSAI status of a company and returns the relevant company details associated with FSSAI certification.

MSME (Udyam) Verification

Verifies the Udyam Registration number (MSME India) and returns relevant details like Company Name, Unit details and Address of the Company.

Book a demo to see how we can help with your verification needs and get a quick proposal.

About

We are your friends at frslabs

FRSLABS is an award-winning research and development company specialising in customer onboarding, identity verification and fraud prevention solutions for businesses. Whether you are a big bank, insurance, telco or a small investment broker, we help you onboard and verify your customers with greater flexibility, compliance and reliability.

Built for you, not for investors

We do what is right for you (and only you) at scale. Nothing is off-limits for us when it comes to innovation, a culture best reflected in the array of patents we have filed. We want to be your trusted partner, to build the solutions you need, and to succeed when you succeed.

Priced for success

We are driven by our mission to touch a billion lives with our tools and not beholden by venture capital or mindless competition. We therefore have the freedom to do the right thing, and price our products sensibly, keeping your success and our staff in mind.

Supported by humans

Whatever it takes, we are here to help you succeed with our products and services. For a start, you get to talk to a human for help, not bots, to figure things out one-to-one. Whatever your needs, however trivial or complex it may seem, we have you covered.

**

.